IRS Section 179

2022 Section 179 in 5 minutes or Less

Questions? 800-322-9738

2022 Deduction Limit is $80,000 (eighty THOUSAND DOLLARS)

Available for new and used equipment, vehicles, machinery, etc., in addition to off-the-shelf software purchases (not applicable for custom software). To use the deduction in tax year 2022, the property must be financed and put into service by end-of-day on December 31, 2022.

BONUS DEPRECIATION: 100% FOR 2022

Bonus Depreciation is in addition to Section 179. Some years it isn’t applicable but in 2022 it is one hundred percent. What that means is that equipment costing more than $1,050,000 can still get the full deduction. Important: Section 179 has always been available for the purchase of new or used equipment but 2022 is the first time that Bonus Depreciation is available to both new and used equipment. Also note worthy is that businesses with a net loss qualify to deduct some of the cost of new equipment and carry-forward the loss.

2022 SPENDING CAP ON EQUIPMENT PURCHASES IS $2,700,000

Spend up to $2,700,000 on equipment. Beyond $2.7 million, the Section 179 Deduction starts to drop — dollar for dollar. This cap makes Section 179 a “small/medium business tax incentive”

(FYI: larger businesses that spend more than $3.7 million on equipment won’t get the tax break.)

HERE IS HOW THE 2022 SECTION 179 & BONUS DEDUCTION WORK.

SECTION 179 QUALIFIED FINANCING

Section 179 and Bonus Depreciation are available for all leases and financing done for equipment, software, building improvements, computers, office furniture/equipment, etc. (qualified assets listed below).

Contact a Taycor Finance Professional today to discuss your needs and how we can help you meet your goals prior to the December 31st deadline.

QUALIFYING PROPERTY & EQUIPMENT

New or Used Equipment, Off-the-Shelf Software, Vehicle for Business Use – weight 6K pounds or more, passenger vehicles capped at $11,160, Computers, Machinery, Office Furniture, Office Equipment, Other Tangible Goods. Most improvements to non-residential building interiors put in service after December 31st, 2017. Other improvements to non-residential buildings such as: HVAC, roofing, security systems, alarms and fire suppression systems. Property must be used more than 50% of the time by the business to qualify for the deduction. Note: new laws allow 100 percent depreciation to be applied to qualified film, television and live theatrical productions.

NON-QUALIFYING PROPERTY & EQUIPMENT

Custom Software, Personal Vehicle (no business use), Certain non-residential improvements (building enlargement, any elevators or escalators, internal structural framework of building, most plumbing, electrical, renewables, lighting, construction, etc.). Note that the following types of property are not eligible for the one hundred percent bonus depreciation: property used in the trade of Electric energy, water or sewage disposal services, gas or steam through a local distribution system, or transportation of gas or steam pipeline, floor-plan financing.

PROPERTY & EQUIPMENT WITH PARTIAL QUALIFICATION

If an item is used for both business and personal, the deduction will apply to the portion of time the equipment is used for business purposes.

Simple Math: Asset Cost multiplied by % Use by Business equals Amount Eligible for tax break.

Property Cost

% of Time Used for Business

The portion of the Cost Eligible for a Tax Break

Note: The property must be used more than 50% of the time for business purposes to qualify. Special rules apply for longer production period property and certain aircraft, consult a tax professional.

| Bonus Savings Example: | |

|---|---|

| New/Used Equipment Purchase: | $ 30,000 |

| First Year Write Off: | $ 30,000 |

| ($1,080,000 = maximum in 2022) | |

| 100% Bonus First Year Depreciation | $ 0 |

| (updated to 100% in 2022. $30,000 – $30,000) | |

| Normal First Year Depreciation: | $ 0 |

| (20% in each of 5 years on remaining amount) | |

| Total First Year Deduction: | $ 30,000 |

| ($30,000 + $ 0 + $ 0) | |

| Cash Savings: | $ 10,500 |

| ($30,000 x 35% tax rate) | |

| Equipment cost after Tax: | $19,500 (35% first yr. deduction) |

| (assuming a 35% tax bracket. $30,000 - $10,500) | |

The above is a 10K foot view of the 2022 Section 179 Deduction, for more details, contact your Taycor Finance Professional.

This website was created to answer questions about the 2022 Section 179 Tax Deduction. We have endeavored to explain these complex tax rules in plain terms; and we’ve attempted to outline what property qualifies under Section 179 for the tax deduction; and we’ve provided specific examples of how this incentive could impact your bottom line. Additional information can be found on the IRS site as well as by contacting a Taycor Finance Professional at 800-322-9738. As always, contact a tax professional before making any important buying decisions.

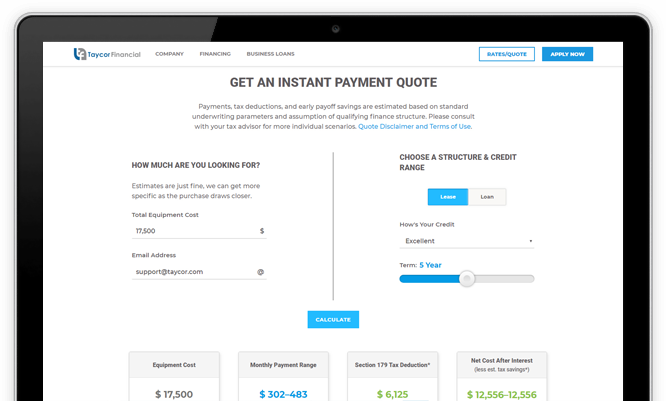

Section 179 Estimator

Below, you will find an illustration of your proposed tax savings based on your selected equipment cost and tax rate.

Total First Year Deduction

100% for 2021

$ N/A

Cash Savings*

based on corporate tax rate

$ N/A

Equipment cost after Tax

Savings Example

$ N/A

The above is a 10K foot view of the 2021 Section 179 Deduction, for more details, contact your Taycor Finance Professional.

This website was created to answer questions about the 2021 Section 179 Tax Deduction. We have endeavored to explain these complex tax rules in plain terms; and we’ve attempted to outline what property qualifies under Section 179 for the tax deduction; and we’ve provided specific examples of how this incentive could impact your bottom line. Additional information can be found on the IRS site as well as by contacting a Taycor Finance Professional at 800-322-9738. As always, contact a tax professional before making any important buying decisions.